Beef: The mechanisms behind the price

Dr Isam Almadani and Dr Zazie von Davier, Thünen Institute of Farm Economics, Braunschweig

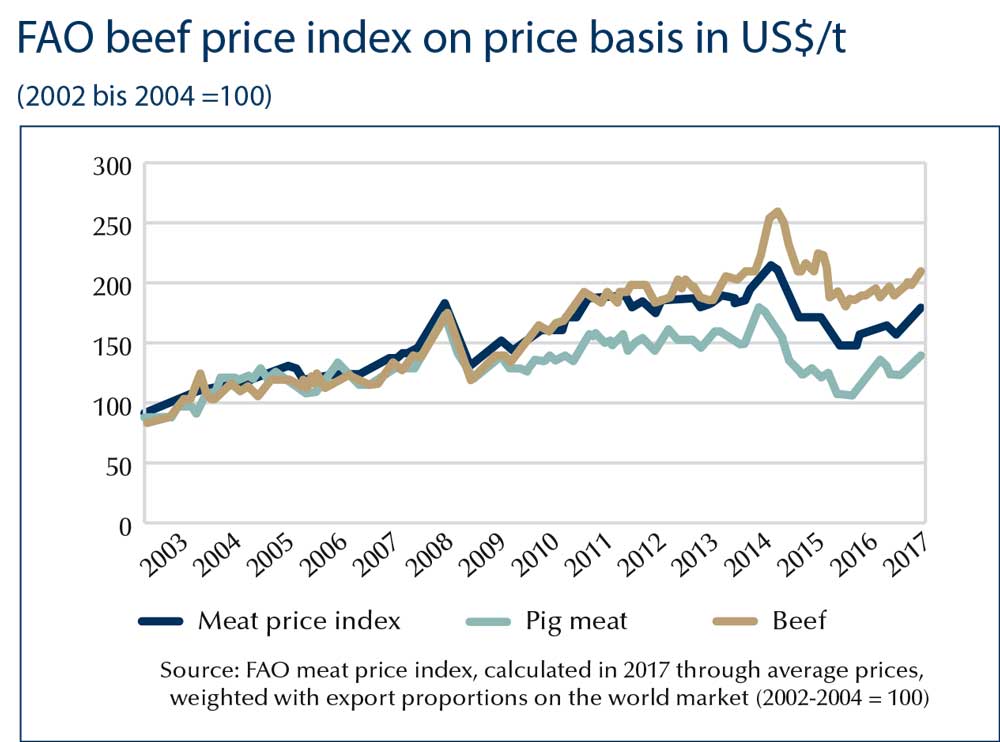

Climate change, government policies and export market access are all important factors influencing the worldwide beef market. Isam Almadani and Zazie von Davier highlight some of the relevant details for us. What are the factors influencing beef production and its pricing structure on domestic and world markets? Is supply and demand alone responsible, or does politics play the greater role in the long term? And what are the effects in this context of the extreme weather events, occurrences we can nowadays expect more often due to climate change? For some years now we've been looking for appropriate answers within the framework of the »agri benchmark Beef and Sheep« network coordinated by the Germany-based Thünen Federal Research Institute. Helping us thereby is information from the agri benchmark databank as well as from offical statistical and trade databanks and - especially important for understanding developments in partner countries - assessments of farmers, advisers and scientists. Recently, regional domestic beef prices have mainly followed price developments on the world market. However, developments haven't been the same everywhere. A glance at some selected regions shows that different factors of influence may apply in respective areas. |

Europe

In recent years the EU market has been influenced by:

- the end of milk quotas,

- the importance of dairy animals for beef production and

- a mainly stable demand for beef.

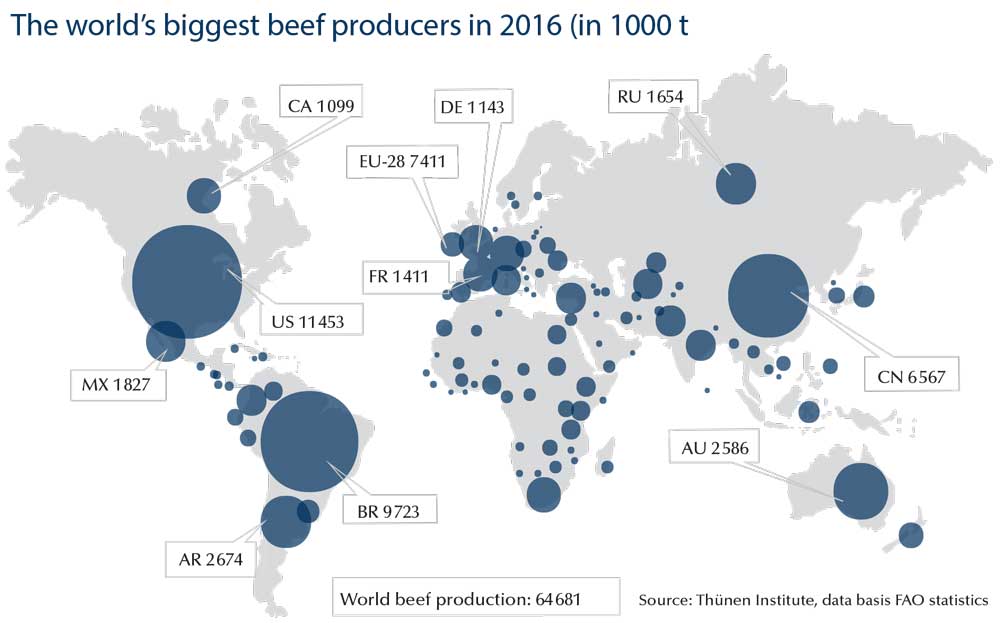

In Europe, milk production and the beef sector are in part closely integrated. From 8 million tonnes (m t) beef produced in the EU during 2018, the EU Commission states that around 2.5 m t came from bull beef production and roughly the same amount from dairy herds. Additionally, important amounts of meat came from heifers (1.4 m t) and from steers (0.7 m t). Removal of the milk quota in 2015 resulted in global overproduction of milk and falling milk prices, with the beef market also affected. For instance, in Germany increased culling of dairy cows meant the 2016 beef price reduced 4% compared to the year before.

This beef from dairy association is especially prevalent in countries where dairy herds, and not a specialised beef cattle sector, produce most of the beef. Among such countries are Germany, Austria, Italy and the Czech Republic. In such a scenario the reduced dairy cow population means less animals are available for slaughter one year later and of course fewer calves are born.

In France and Spain, the proportion of specialised beef breed herds is substantially higher than in the aforementioned countries. But also there, the effect of milk quota removal still left its mark on beef prices. Ireland, a country where beef production is mostly based on grassland, also experienced beef price pressures because of the oversupply of slaughter cows on the EU market.

What influence have consumption trends?

In Germany, for example, the 2017 increase in per capita consumption of 0.4 kg to 14.6 kg helped influence an increase in beef price, despite beef imports from Brazil and Argentina increasing at the same time, in part because the increasing domestic consumption. However, increasing or comparatively high consumption figures for beef are not to be found everywhere in the EU. In Poland, for instance, annual per capita consumption lies under 4 kg. There, the 2017 beef price maintained a comparatively high niveau. While the Polish farmers' price for beef may seem low to producers compared with comparable international figures, for the consumer beef is still too expensive compared with poultry and pig meat.

The drought conditions in many parts of Europe and resultant feed scarcity led in 2018 to more beef landing on the market, mainly through cow and heifer slaughter. This action slightly reduced EU cow numbers compared to the previous year while prices for live animals and beef dropped markedly on the year.

North America

Recent important influences on prices for the region comprised:

- Canada's high exports (40 % of beef production shipped abroad) with a simultaneous

- increase in the importance of the USA as sales market for Canada (more than 70% of exports), as well as

- expansion of beef cattle output in the USA.

Beef production in the USA (12 m t) and Canada (1.3 m t) is closely linked. In 2015, May store calf prices in Canada reached record heights, only to collapse by up to one-fifth by the end of that year. The downward trend continued until September 2016, a development caused by a combination of influences. Deliveries in the USA crashed in 2015 and 2016. However, Canada's southern neighbour is its biggest beef customer (on the hoof as well as on the hook). This development increased the offering of cattle and beef on the home market, without any significant effect on herd size. As a result, the price for live animals dropped into the cellar. In the following year exports of store calves remained modest, although greater international demand for beef boosted exports by 6%. This eased the market in Canada and prevented a decline in producer prices.

In 2018, low live animal exports and increased domestic production stood against increasing demand for beef from export markets. Economic expansion in various export destinations and the outbreak of African swine fever in China supported international demand for beef. Higher numbers of feeding cattle and a rise in feed prices dampened subsequent price development, however.

In the USA, record prices in 2014 and 2015 as well as the good economic situation in beef cow production led to a marked expansion in output, which than resulted in a substantial price drop in 2016. In 2017, the price remained relatively stable with sales being boosted through markedly reduced slaughter weights, high domestic demand and increasing US beef exports (above all to Japan, South Korea and Hong Kong). Feeding cattle numbers in the USA rose in 2018 for the third year in succession. Calf numbers also hit the highest level since 2007. In total, the amount of beef on offer also rose. Despite this, beef price in the USA has not dropped over the respective years because a strong international demand supports prices.

Alongside trading relationships, currency exchange developments also influence beef prices. The continual rise in prices in Mexico, where around 18% of US beef exports landed in 2018, went hand-in-hand with devaluation of the Mexican peso and the expansion of grain-based beef production in feedlots. Once again, this led to improved competitiveness on this export market.

South America

For South America in recent years, three factors have proved of great importance:

- the political situations,

- currency exchange effects (on exports), and

- pronounced drought periods.

In the eyes of European cattle farmers, Brazil and Argentina are often the countries where »milk and honey flow«: with great expanses of land and supposedly low production costs and less stress from bureaucracy. However: profit and loss of South American beef cattle producers depend very strongly on political decisions - and these don't always stand on the side of beef farmers.

Over recent years in Argentina the most important factor of influence in price developments for live animals and beef has been the political instability. Its effect could be seen in pronounced devaluation of the Argentine peso, annual inflation of more than 30% and lifting of the beef export ban with beef exports increasing strongly from a low level and the domestic price of beef soaring. This then affected the domestic consumption of beef.

Argentina's droughts in 2017/18 led to lower weaned calf numbers and high numbers of cows slaughtered for export. Additionally, the marked devaluation of the national currency in 2018 led to 20 - 30% lower beef prices, when converted to US dollars, which substantially improved the international competitiveness of Argentinian beef.

In Brazil, beef prices reached a record level in 2015. As in Argentina, the reason lay in increasing inflation and devaluation of the currency as consequence of political and economic instability. Added to this were the effects of a massive drought in 2014 and 2015 in Brazil's most important grassland areas (over 96% of beef production there is pasture based). The drought occurred in the breeding season, so that in-calf rates slid back drastically.

Because of the long reproduction cycle in cattle, the results of such events make themselves felt with a marked time lag in the slaughter cattle market. So, for instance, the number of cattle slaughtered in 2016 was 13% down on 2014. At the same time, calf prices showed a record increase of 40% and prices for bulls and steers also rose steeply with corresponding effect on the price of beef.

In 2017 Brazil's largest beef processor and exporter JBS came under suspicion, along with others, of having sold contaminated meat. The »Operation low quality meat«, which resulted in several dozen meat inspectors losing their jobs, had important negative influence on the credibility of meat processors and also affected their slaughter and processing throughputs. The reduction of slaughter capacity and the oversupply of fattened animals carried a slight price reduction in its wake. On top of this, the Brazilian cattle herd had recovered from the 2014/15 drought and this was reflected in sinking calf prices in 2016. In the opposite direction, the revaluation of the Brazilian real at 8% against the US dollar led to higher beef prices when measured in dollars.

Last year the beef price in Brazil was slightly lower than that of the previous year. As in Argentina, devaluation of the domestic currency compared with the US dollar boosted exports, supported also by rising beef demand in Asia. Beef exports ended up 19% over the previous year at 500,000 t.

Australia

The theme »drought« has the greatest influence on the beef sector in Australia, the land mass most strongly affected from the climate events »El Niño« and »Indian Ocean Dipole«. Australian beef production in 2018 totalled 2.3 m t with around 70% exported. The four-year 2013 - 2016 drought has been one of the longest, most intense and extensive experienced since 1885. Cattle population sank by 11%. The end of the drought period saw record prices being paid for livestock and for beef. In 2016, the live animal price rose by a quarter, after doubling in the previous three years.

In 2017 there followed in the most important production regions a season with below average precipitation and high average temperatures so that investments in herd restocking were hesitant and still more cattle ended up on the market. The poor condition of grassland meant increased supplementary feeding. All this influenced the beef price negatively.

Again in 2018, less than adequate rain fell on most of the main beef production regions in Australia. Cattle farmers were beset by rising feed costs, poor pasture condition and limited possibilities for feeding all of their cattle adequately. As a result, cow slaughter numbers soared to new heights and price pressure increased. This situation once again heated-up competition between Australia, the USA and Brazil in the supply of beef to important export regions.

How drought affects the market

Here’s a general example of how beef prices are influenced by drought conditions:

Lack of rain and resultant reduced forage availability, lower grain yields and consequently increased supplementary feeding mean higher feed costs and/or culling requirement in herds. This last action brings more meat onto the market and pulls down beef prices.

Reducing herd size has the unavoidable time-lagged effect of less calves produced, reducing beef supply and increasing market prices in the future. The period of higher meat prices lasts through to the end of the drought.

When rainfall starts and there’s expectation of better forage harvests, cattle farmers are encouraged to restock their herds. Females are retained as replacements in the herd. Result: reduced numbers of livestock, including slaughter cattle, come onto the market so that prices continue at a high level.

Africa

In Africa too, aridity trends have had great influence on beef production developments.

In Namibia and South Africa, the 2016 recovery from the preceding three years of drought led, as in Australia, to herds restocking, thus reducing availability of feeding and breeding cattle as well as increasing beef prices. That year (2016) saw South Africa becoming a net exporter of beef for the first time. In Namibia, the limited availability of cattle was exacerbated by weaner calf exports to South Africa increasing by 50%, all of which led to high cattle prices.

A marked period of drought also hit Morocco in October 2015, especially affecting the main production regions for beef and grain. Morocco's exports of grain including wheat sank by 70% on the year in 2016 to the lowest figure since 2007. This situation forced beef producers to cull their headage by up to a half in order to cover the expenses of keeping the remaining livestock. The consequent increase of meat on the market dragged beef prices downwards. The drought period continued into the 2016/17 harvest year, although less extreme than in the previous 12 months.

Favourable weather conditions in 2018 included sufficient rainfall in South Africa and Namibia and led to good beef prices, supported by increasing export trade. This also applied in Morocco where satisfactory feed availability and a record grain harvest meant no forage scarcity and plenty homegrown concentrate rations, which in turn avoided any emergency culling. A 10% higher price level was recorded.

Summary

In an increasingly globalised beef market, market developments depend on numerous influences. Even events at the other end of the world have an influence on the way the beef markets in our own countries develop.