European Pig Producers (EPP): Country Report Netherlands

Market situation

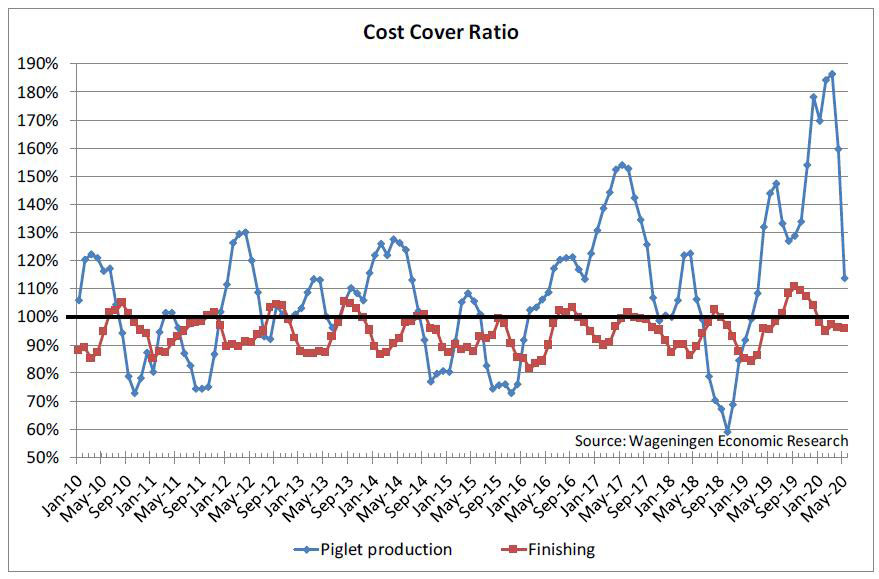

Pig farming increasingly becomes challenging, as price fluctuations are stronger than before and market disturbing events seem to happen more often than in the past. African Swine Fever brought high market prices in 2019 and a positive outlook for 2020. However, Covid-19 has disturbed the expectations. In May Covid-19 was found in employees of several slaughter and processing plants in the Netherlands. A few plants were closed, one day, a week or up to two weeks. This led to reduction of slaughter capacity, but up to now this could be solved by other plants. An effect of Covid-19 is found in lower market prices than expected, due to less demand for pig meat from the food service, as well from southern European processors. Especially the more expensive parts of the pig are less demanded now. Although export to eastern Asia is possible, the market price is under pressure. Still, as Covid-19 is not disturbing production capacity and there is sufficient global demand for pig meat, we expect the market to recover rather quickly. In that perspective Covid-19 is only a small turbulence, compared to African Swine Fever. The meat industry is working hard on preventive measures for their employees against Covid-19, and meanwhile keeping prices on a constant level, to not give pace to panic. All in all, we still deem it possible that 2020 becomes a rather positive year for pig production. Recovery of the global pig production will take a few years. Prices for slaughter pigs were a bit over 1.50 euro/kg (hot) carcass weight (ex.VAT) in May, down from a level just over 2 euro/kg in March. This steep reduction is due to limited sea transport logistics (cool reefers were stuck in Chinese harbours), and lower valorisation of high-end pig meat products, and reflects uncertainty for all stages in the supply chain as well. Piglet prices, typically reflecting market expectations for pig meat in the next 4 months, fell from about 95 euro in March to just over 50 euro per 25kg piglet in May, far more than some 5 euro price drop in that period according to the seasonal pattern. Graph 1 shows the monthly cost cover ratio in piglet production and finishing. The long-term ratio (2010-2018, more recent data left out) has been 104% for piglet production and 94% for finishing on average. Latest cost coverage amounted to 114% in May in piglet production (down from 186% in March) and 96% in finishing (slightly lower than 97% in March), so rather average profitability figures. Especially piglet producers are facing strongly fluctuating ratios and have lost quite some profitability.

Feed prices are increasing. The current price level (May) amounts to €270 per ton of complete feed for a closed cycle farm, up from €258 per ton in October last year. See Graph 2.

Government

The Dutch government initiated the voluntary Saneringsregeling, aiming to buy-out farms with odour nuisance for citizens. Farmers recently received a letter from the government in which they are told whether they are accepted for the buy-out scheme and what payment they will receive. Still we expect some part of the farmers to finally not joining the program, but proceeding with their farm. Those who agree will have to stop production within 8 months after receiving the governmental letter. We expect a reduction in number of pigs in the period from Christmas 2020 till Spring next year. The reduction will amount to 5-7% of the pigs and maybe more, as additional budget is foreseen. The reduction is likely to be a bit higher in sows than in finishers.

The Ministry of Agriculture also sent an ambitious plan to the Parliament for reduction of Nitrogen surpluses on nature areas. This also includes further reduction of animal husbandry. Plans are still too vague to estimate consequences for the pig sector.

June 2020

Robert Hoste, EPP Dutch Branch and Senior Pig Production Economist at Wageningen Economic Research