ISN Slaughterhouse Ranking 2020: Major Challenges Due to Corona and ASF

2020 was a special year for the entire pig industry. With the Corona pandemic, African swine fever (ASF), the backlog supply of pigs, the closure of restaurants, the ban on third-country exports and the abolition of work contracts, 2020 was quite turbulent for the entire industry - including the slaughter companies. Overall, the crisis has further accelerated the long-standing trend: Fewer and fewer slaughter companies are competing for a decreasing number of German pigs for slaughter. The discussion about margins must now be brought to a conclusion!

When evaluating the 2020 ISN slaughterhouse ranking, it must be taken into account that the Corona pandemic had a considerable impact on the number of slaughters per slaughterhouse, depending on how the respective slaughter locations were affected. Despite the crisis, however, the shifting within the ranking was rather unimportant.

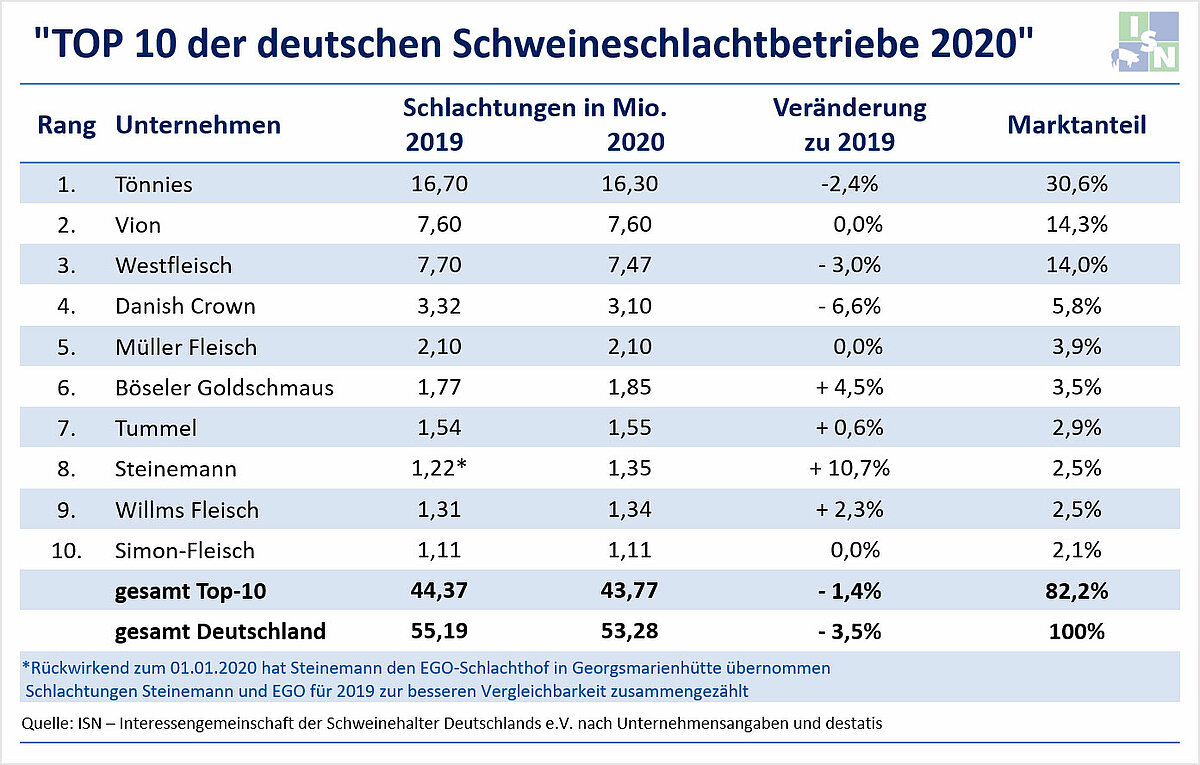

A total of 53.28 million pigs were slaughtered in Germany last year. That was 1.91 million animals or 3.5% fewer than in 2019 - the lowest figure in 14 years. All in all, the top 10 slaughter companies slaughtered 82.2% of all pigs in Germany. In 2019, the figure was still 80.4 %. Some medium-sized companies merged. The concentration in the slaughter industry has therefore continued to increase.

Last year, the Tönnies company slaughtered 16.3 million pigs in Germany - about 400,000 animals or 2.4% fewer than in 2019.

The decline thus was less than that of the market as a whole and Tönnies was able to increase its market share by 0.3 % to 30.6 %. This is remarkable because, after all, the largest Tönnies slaughterhouse in Rheda-Wiedenbrück (with approx. 130,000 pig slaughters per week) was completely closed for four weeks from mid-June following numerous positive Corona tests among employees. Even after that, slaughtering and cutting operations there were severely reduced for another 18 weeks. The Tönnies site in Sögel was also severely restricted for weeks. It was precisely the restrictions in Rheda-Wiedenbrück that triggered the pig shortage, which extended to over one million pigs by the end of the year.

The Dutch slaughter company Vion regained second place in the slaughterhouse ranking. With 7.6 million pigs slaughtered in Germany, the company was able to keep its annual slaughter volume stable compared to the previous year. Vion was also affected by the Corona pandemic, with significant restrictions at individual slaughterhouses, but was apparently able to compensate for this through its slaughterhouse structure spread throughout Germany. Vion's market share increased by 0.5% to 14.3%.

The cooperative slaughter company Westfleisch recorded a decline in slaughter volumes of 3 % to 7.47 million pigs last year. Westfleisch also had to cope with restrictions in slaughterhouse capacities due to the Corona pandemic. For example, the Westfleisch slaughterhouse in Coesfeld was the first major slaughterhouse to have to take a temporary break. However, because the decline in annual slaughter volumes in the company was similar to the decline in the market as a whole, the market share remained unchanged at 14 %.

The companies in positions 4 to 10 were largely able to maintain or even increase their market shares. Böseler Goldschmaus, for example, was able to increase the number of pigs slaughtered in 2020 by 4.5 % compared to 2019. An exception was the only German slaughter location of the Danish slaughter company Danish Crown in Essen (Oldenburg), where a considerable decline in slaughters of 6.6 % was recorded.

A newcomer to the list of the top 10 slaughter companies in Germany this year is Steinemann from Steinfeld in Lower Saxony, which took over the slaughter company of the Osnabrück producer group in Georgsmarienhütte.

The already significant reduction in the number of pigs in Germany was accelerated by Corona and ASF. For the slaughter companies, German pigs will thus become scarcer in the future, which is likely to lead to structural changes in the slaughter industry. Further closures, especially of smaller and medium-sized slaughter companies, as well as further takeovers or mergers could be the result, so that concentration is likely to increase further. For the slaughter companies, securing raw materials for pigs is becoming increasingly important - both quantitatively and qualitatively.

There is no doubt that the costs of the slaughter companies have risen, among other things due to the Corona pandemic last year. However, the known annual financial statements of slaughter companies also clearly show that - in contrast to pig farmers - they have financially survived the crisis year 2020 very well. Here, the distribution of revenues in the chain has been seriously disrupted to the detriment of the pig farmers.